Inheritance tax (IHT) is a tax paid when your estate is worth more than £325,000 at the time of your death. Such IHT payable can be reduced when you carry out a good plan.

Here are some important tips that can help you reduce the taxman’s cut.

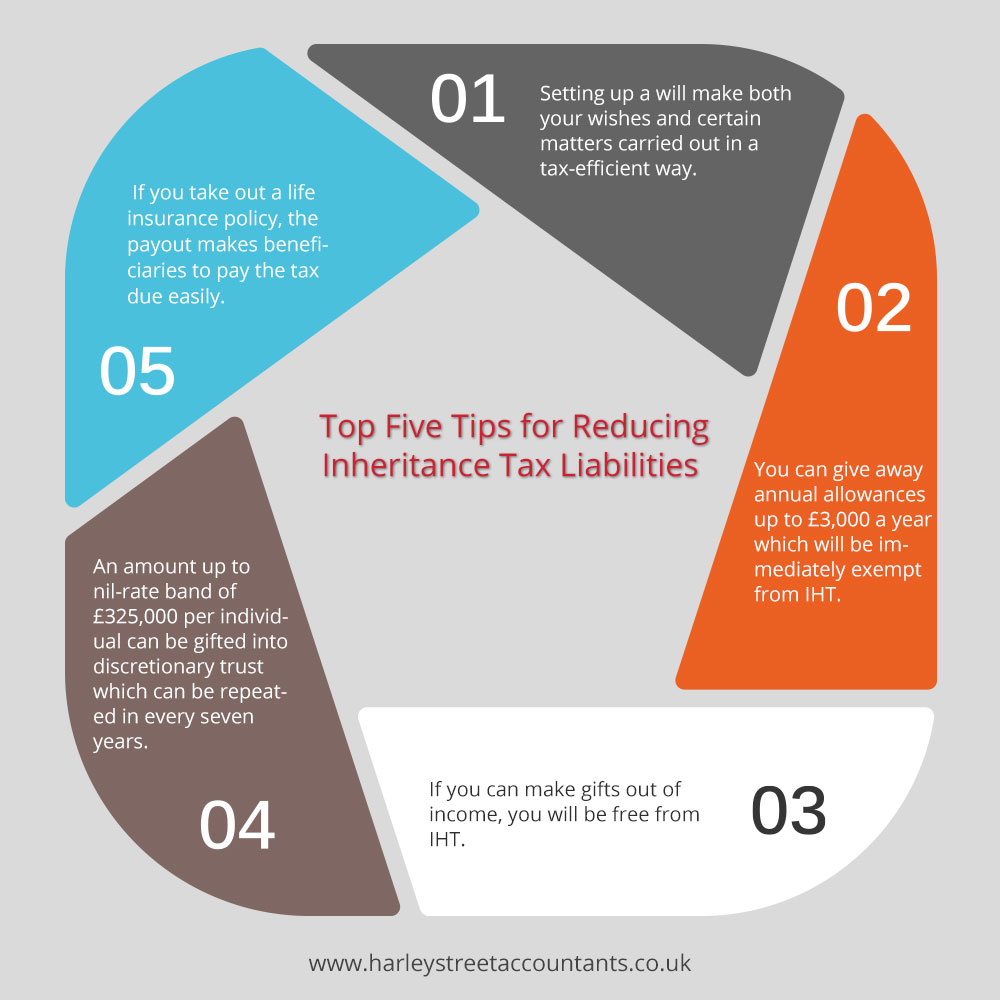

Set up a will

Setting up a will make both your wishes and certain matters carried out in a tax-efficient way. This means you do not have to rely on intestacy rules that come into play where there is no will.

If you are not married but have considerable assets, you need to consider setting up a will. It is because under the intestacy rules, IHT liability would pass on to your parents and not your brothers or sisters.

If you are married, your death can lead to a financial anxiety for your better half since the law decides what to do with your estate. There is also another problem of a possible immediate charge to IHT.

Take advantage of exemptions

You can give away annual allowances up to £3,000 a year which will be immediately exempt from IHT. Likewise, you can give up to £250 to people as it is also a small gift exemption

Wedding gifts up to £5,000 for parents, £2,500 for grandparents and £1,000 for everyone else, donations to qualifying charities are also exempt from IHT.

The cash gifts and assets worth more than the annual allowance will automatically be exempt especially when you survive for seven years from the date of gift given.

Make gifts out of excess income

If you can make gifts out of income, you will be free from IHT. However, these gifts only qualify if they form part of normal expenditure, made out of income and shouldn’t affect your living standard. As the executors of your state are the ones who claim this exemption, you need to keep the records of such gifts.

Put things to use trusts

An amount up to nil-rate band of £325,000 per individual can be gifted into discretionary trust which can be repeated in every seven years. Although more can be gifted, you need to note that the amount above the allowance would earn a lifetime transfer tax of 20 per cent. CGT rollover, control over the assets, protection from beneficiaries or former spouses or creditors claiming through them are allowed by trusts.

Take out some life cover

If you take out a life insurance policy, the payout makes beneficiaries to pay the tax due easily. So, when death takes place, the payment of the death benefit will happen immediately and the funds will be available for paying the tax without waiting for grant of probate.

If you are worried about your IHT, it is recommended you seek a inheritance tax advice from professional accountants.