Doing your own financial books may seem a bit difficult than you imagine. But, that shouldn’t stop you from doing it. As bookkeeping is a very important part of your business, here is a breakdown of tips for doing it on your own.

Keep your financial records

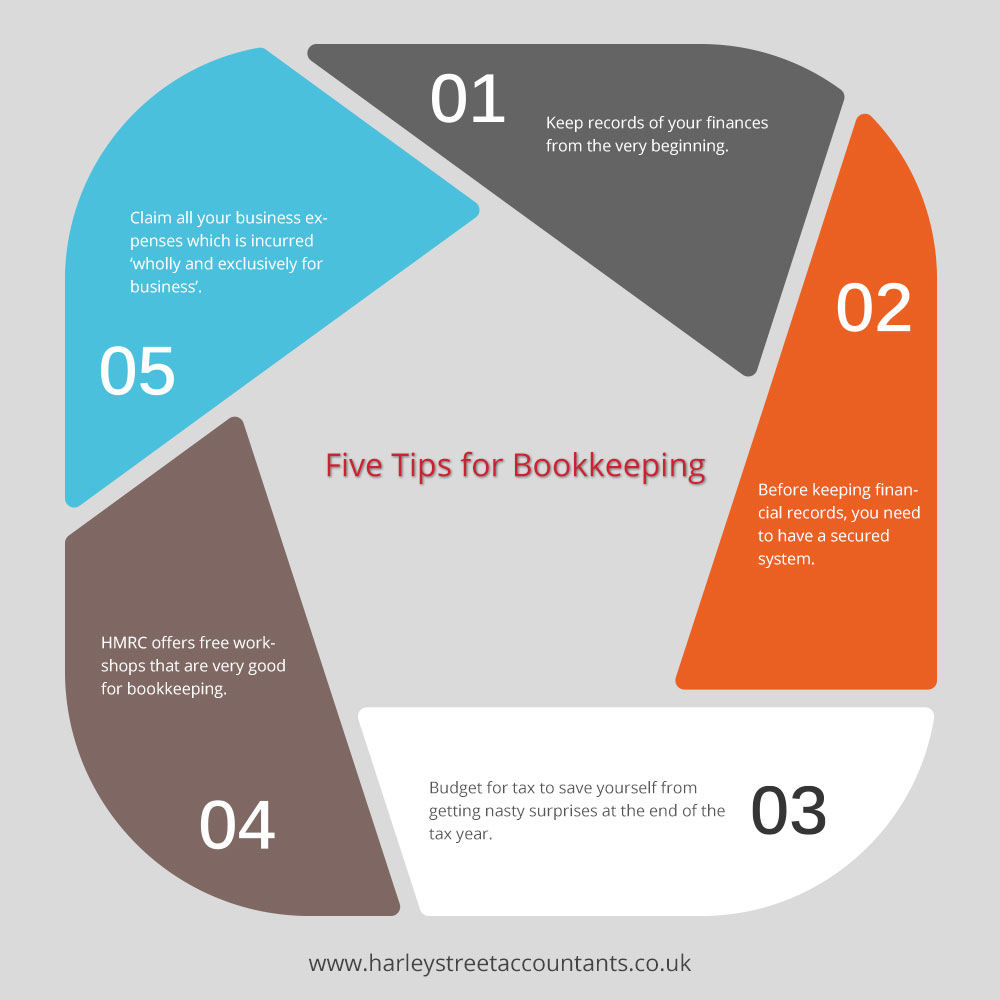

Keep records of your finances from the very beginning. Along with the updated financial information, remember all the important dates for paying tax or VAT. In case, if you do not meet the deadline and make late payments, costly penalties can be incurred to you.

Get a secured system

Before keeping financial records, you need to have a secured system. You can either use software packages or manual system. But, using a latest software package is a wiser option. If you intend to use accountants, you can ask about them about the system and then agree to use it before starting business or ask them if they offer a ready-made spread sheet.

Plan for tax payment

Cash flows of your business should be managed correctly because you have to pay a part of your income to taxman. That is why you need to budget for tax to save yourself from getting nasty surprises at the end of the tax year. For budgeting, open a savings account and put around 20-30 percent of your income for paying your tax bill.

Make use of HMRC resources

If you think HM Revenue & Customs (HMRC) doesn’t offer free things, wait till you read further. HMRC offers free workshops that are very good for some like you who is doing your books. These workshops include employer online filing and running a payroll, introduction to VAT and international trade, becoming self-employed and setting up a limited company and many more.

Claim for all business expenses

You can claim all your business expenses which is incurred ‘wholly and exclusively for business’. Even the smallest costs including stamps, travel expenses can make a difference so, make sure you include all of these receipts.

If you are using home as your office, you can still claim for your expenses including lighting, heating, telephone and internet. Moreover, even a percentage of rent or mortgage interest can be claimed but that cause you to pay Capital Gains Tax. If you are not sure about this whole thing, you can speak to your accountant and ask for suggestions.

Managing your bookkeeping can be tricky if you do not follow some important rules. So, take charge from the start and do all of the above mentioned things to ensure you are on the right track.